The Conceptual Framework for Financial Reporting 2018

- Muhammad Shazaib

- May 20, 2019

- 6 min read

Ever wondered what does this heavy phrase "The conceptual framework for financial reporting" mean?

I have always been wondered with what actually the conceptual framework for accounting is until I dug into this.

What is it?

In simple words, the conceptual framework for financial reporting ("the Framework") is a basic document that sets objectives and concepts for general purpose financial reporting.

We need to make one thing clear in mind that the framework is not an accounting standard, rather acts as a guide for the preparers of the financial statements. It acts as a tool for the management to use judgment in applying accounting policies where a specific standard is not applied.

History

In 1989, the Framework for the Preparation and Presentation of Financial Statements was issued by International Accounting Standards Committee (ISAC) which is now known as the International Accounting Standard Board (IASB).

But, then the IASB made amendments to it and the new and finished framework was issued with a new name The Conceptual Framework for Financial Reporting in 2010.

It stayed in progress for many years and in March 2018, the ISAB issued the final version of the framework which is called The Conceptual Framework for Financial Reporting 2018.

Why did the IASB revise the Framework?

The previous versions of frameworks were useful but incomplete and required improvements:

There were Filling Gaps. For example, guidance on measurement, presentation, and disclosure was missing.

Updating. For example, the definition of an asset and a liability.

The changes?

The major changes that the ISAB made were:

Measurement: concepts on measurement, including factors to be considered when selecting a measurement basis.

Presentation and disclosure: concepts on presentation and disclosure, including when to classify income and expenses in other comprehensive income.

Derecognition: guidance on when assets and liabilities are removed from the financial statements.

Let's Get Started

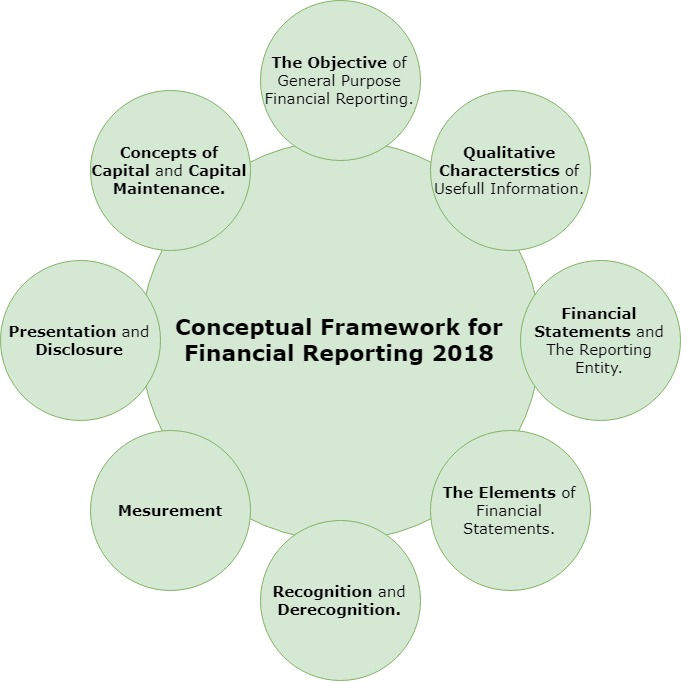

The new framework has 8 chapters in total and here is the list. We will look at each of these in detail.

The Objective of general purpose financial reporting;

Qualitative characteristics of useful information;

Financial statements and the reporting entity;

The elements of financial statements;

Recognition and derecognition;

Measurement;

Presentation and disclosure; and

Concepts of capital and capital maintenance.

The Objective of General Purpose Financial Reporting

The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to the existing and potential 1) Investors, 2) Lenders and 3) other creditors to make various decisions. For example about the trading of debt and equity instruments.

So what financial information should a reporting entity report in the general purpose financial reports?

The entity should present financial information in the general purpose financial reports about the economic resources and claims. In simple words, this is the statement of financial position of an entity.

The entity should also report changes in economic resources and claims resulting from financial performance and other events. In simple words, we are talking about the statement of profit and loss and other comprehensive income.

The financial performance should be reflected by accrual accounting.

The entity should also present financial performance resulted from past cash flows.

Qualitative Characteristics of Useful Information

Chapter two of the framework discusses the qualitative characteristics of useful information and there are two types of characteristics:

Fundamental: The first fundamental characteristic is Relevance. Relevant financial information is capable of making a difference in the decisions made by the users of financial information. Here the concept of Materiality applies. So the material information must be presented in the financial information and should not be omitted. The second fundamental characteristic is the Faithful representation. Information should be faithfully represented, meaning that, it should be complete, neutral and free from error.

Enhancing: The useful information should have both fundamental as well as Enhancing characteristics. Here the meaning of enhancing characteristics it should be:Comparable - between entities and different time periods.Verifiable - Knowledgeable users should be able to verify the information with given sources.Timeliness - The information should be available in time to the users so that timely decisions can be made. Understandability - The information should be classified, presented clearly and concisely.

Financial Statements and The Reporting Entity

Chapter 3 discusses the financial statements and the reporting entity. We all are pretty familiar with this chapter from the very early stages of our studies. Let us take a quick recap.

Here we are talking about the full financial statements but not only the reporting itself. The entity presents relevant information in the Statement of Financial Position by recognizing Assets, Liabilities, and Equity.

The financial performance is provided in the Statement of Financial Performance by recognizing Income and expenses.

And, the entity reports financial information in Other Statements where information about elements of the financial statements, cash flow of the entity, assumptions and estimates used, and contributions made by shareholders/ owners, and distributions made to the shareholders is presented.

Chapter 3 also discusses the Reporting Entity. The financial statements can be prepared by:

A single entity.

A portion of an entity.

More than 1 entity.

Note that the reporting entity needs not to be a Legal entity!.

The reporting entity can present its financial statements in the following way:

Consolidated - Where there is a relationship between parent and subsidiary and the financial statements are presented as a single entity.

Unconsolidated - Where information is only presented for a single/ parent entity.

Combined financial statements - This is where there is no relationship between parent and subsidiary but the entities are somehow related to one another. For example, the entities are owned by one shareholder.

Financial reports are always reported for a specified period of time and on a going concern basis. This means that the entity will continue its operation in the foreseeable future.

The Elements of Financial Statements

We are also very familiar with this chapter. The chapter discusses the elements of the financial statements i.e. statement of financial position or traditionally called balance sheet, statement of profit (Income statement) and loss and other comprehensive income. Chapter 4 also discusses the statement of changes in equity, where equity-related transactions reported and statement of cash flows. I will not go into detail since we already know about these statements.

Recognition and Derecognition

This chapter is newly incorporated by the IASB. Although different accounting standards have already given us guidance on the recognition and derecognition of elements of financial statements, the framework incorporated the definition and criteria in this framework where guidance is not available in the specific standards.

As per the framework - Recognition is the process of incorporating into the balance sheet or income statement an item that meets the definition of an element and recognition criteria:

It is probable that any future economic benefit associated with the item will flow to or from the entity; and

The cost or value related to that item can be measured reliably.

Derecognition is the process of removal of an item from the balance sheet or income statement and the criteria to remove the element from the financial statements is the same as mentioned above.

Note that, the general definitions of elements of financial statements i.e. Assets, Liabilities, Equity Income, and expenses are very important before an element can be recognized or derecognized.

Measurement

Chapter 6 talks about measurement.

Recognition means when and whether to recognize in the financial statements while measurement means in what amount the element should be recognized.

The framework has presented two measurement basis of accounting.

Historical costs - which is actually the transaction price of an item; and

Current Value - this is subdivided into following.

Fair value.

Value in use.

Current cost.

Note that while using the measurement basis of an item we need to consider the relevance and faithful representation of financial information.

Presentation and Disclosure

Here the concept of effective communication is very important since the presentation and disclosures act as a communication tool for the users of financial information.

The communication in the presentation and disclosures in the financial statements will only be effective if it focuses on the objective and principles of the presentation and disclosure but not merely the rules.

Moreover, the classification in the presentation and disclosure is also taken care of. Meaning that similar items are grouped and dissimilar items are separated.

Concepts of Capital and Capital Maintenance

Finally, the framework laid down the concepts of capital and capital maintenance. However, this chapter is copied from the previous versions of frameworks and there is nothing new here.

The framework explains two types of capital:

The Financial Capital - Which is basically the net assets of an entity. The profit is calculated as the difference between net assets at the end of the period and net assets at the beginning of the period after deducting contributions.

Productive Capital - This is the productive capacity of the entity based on, for example, units of output per day. Here the profit is earned if physical productive capacity increases during the period, after excluding the movements with equity holders.

This is all!!!

Want to know about me?

My name is Muhammad Shazaib and I am a Chartered Certified Accountant having more than 5 years of international working experience in Audit, Accounting, and Value Added Tax in Pakistan, United Arab Emirates (UAE), and Malta (Europe).

LinkedIn profile: https://linkedin.com/in/mshazaib/

Comments